It is very difficult to appreciate that

this is in fact a triple witch expiry, or quadruple as the US likes to call

them, as the activity remains so low.

The level overall is much more befitting

a biggie, but it all looks passive.

And, we are back to that ridiculously

wide zone.

However, and as we pointed out, the

bottom boundary is hugely significant.

Last Thursday, the 23rd, this

index got as low as 25328 before finishing at 25490.

At the time we mentioned how

statistically irrelevant 10-points is on a twenty-five-thousand-point index,

and the opening gap up the next day just went to underline this.

The fact that the next day, Friday, the

intraday low was 25496, was also very telling.

So, yesterday, it was looking good, but

right towards the end the market got spooked, and, hey presto, strike 3.

The only good news is that the next

level of support is actually rather close, and it jumps straight in at R2,

please see above table.

Otherwise, it’s going to be all down to

the SPX, please see our previous comment on the 21st May, and from

our calculations on the 28th R2 here is still at 2770.

The expiry still has a very long way to

go, but it is heating up nicely, and now we are testing levels, both in this

index, the DJX, but also the SPX, this will ignite activity, if only because of

the dynamic delta, so the fun starts now, for us at least.

Nb. Our comment from 05/17/19 (Not published online)

Range:

Activity:

Type:

Nb. Our comment on 05/22/19

The FTSE is a classic example of the

expiry of one month (May) leaving another (June) in a difficult position.

For May, where the zone was 7350-7450 at

the end, it was a tremendous achievement for this index to claw itself all the

way back up from R1 at 7150 (intraday and expiry low 7150.89 13th

May) to get to consecutive closes of 7353.51 and 7348.62 on the final two days.

Well done.

The trouble, as is plain to see, that in

June the zone was, and still is, 7150-7250.

And just to compound that, the ratio

above it is already R3.

So, June has been born into a very high

level of ratio.

No wonder it doesn’t know which way to

turn.

Will it be necessary for this index to

test DR at 7450, who knows?

As it stands, to us it doesn’t appear as

if it has the bottle, as 7350 seems to be a tough hurdle, and this is only R3,

which is what it’s in anyway.

It is not beyond the realms of

possibility, but, as is also very plain to see, the ratios above the zone are

far far greater than those below it.

Therefore, if it does, and 7550 is not

impossible, as triples often go between the B ratios, or at least did a while

back, we see this as only deferring the inevitable.

The real issue for us, in the five weeks

that lie ahead in this expiry, is whether the bottom boundary of the zone will

hold.

As, looking at it as it stands, the next

ratio support level doesn’t kick in until 6950.

And, as this index is already ploughing

through R3, then we doubt R2 will provide that much support.

The next few days should clear things up a great deal, but if we are to get a DR to DR expiry, and don’t forget May traded between the R ratios, you could be looking at a range of 600-points, which definitely deserves a wow wee.

Nb. Our comment from 05/17/19 (Not published online)

Range:

Activity:

Type:

Nb. Our comment on 05/21/19

In our last comment covering the May

expiry we said we expected to see the zone there finish at 2845-2855, which it

duly did.

The reason we mention this, is because

this expiry, the June triple, is still at the old level, but this is purely due

to the fact that these “biggies” just aren’t so nimble on their feet.

So,

even though it hasn’t changed, please take it for granted that the zone here

should be 2845-2855.

And, although it has just been two

trading days, since we last looked at the ratios there have not been many

changes.

Therefore, the fact that so much Y ratio

persists below the zone is not a good thing, and until the zone changes, this

will retard development undoubtedly.

Also, don’t forget this is a five-week

expiry.

Put these two elements together, and you

will, and currently do, have, 135-points of Y ratio.

And in a triple.

To put this into perspective, normally

we would not expect to see any at all.

On top of this, you should be aware that

the serious R ratios below the zone, do not start until the low 2700’s, and

then, they only go up to R3, an incredibly long way shy of the B level ratio we

would expect to see in a triple.

Above the zone, it is slightly better,

but it still only gets as high as DR ratio, so far from ideal.

So potentially a fantastic trading

expiry, but for asset managers probably a worst-case scenario, as with the

trading range in the Y ratio alone of 2795 all the way up to 2930, you have

nigh on a 5% range.

Assuming this is one-way, as more than

likely, just as in May, it will be one way, than a reverse to cover the other

way, before reversing again for the finish, so easily 10%.

Get your timing wrong when you are considering this degree of percent and it will not look pretty, but for traders, it should be great fun.

Already it seems the zone here in the

FTSE is having a major impact.

On Friday last week the intraday high

was 7442.39, and we are more than happy to call that strike one of the zones upper

boundary.

And, yesterday, the market basically

camped out on it for the last two and a half hours of the trading day, so

definitely strike two.

For the record the actual intraday high

was 7456.49.

Interestingly, the ratios above and

below the zone have slipped.

Below R2 slides to 6900, whereas above

both R3 and DR move out by 50-points.

Nevertheless, the situation remains the

same, as in we believe the best place for this market is in its zone (7350 to

7450), as above it R2 is still waiting to ambush it at 7550, whereas below we

don’t even see the R ratios start until 7050.

So, all in all, if it can hold within its zone, we think it will be doing well, as if it gets aggressive it could easily get a bloody nose, and if that shakes loose the bears then it is a long way down before it will find any ratio support.

Range:

7350 to

7450

Activity: Moderate

Type: On balance not bullish

Nb. Our comment on 05/13/19

As you can see from our comments above,

back on the 30th April, the market was all about the upper zone

boundary at 7450.

At that time, we hoped it would stay

within its zone, and it almost did, as the remainder of that week, it was all

about the lower zone boundary.

The intraday high on the 30th

was 7451.32, then on the 1st it was 7446.46, followed by a spike

down to 7339.45 but the close on the 2nd was at 7351.31, and most of

that day was spent in or around the lower zone boundary.

The intraday low on that Friday was in

fact 7350.01.

Of course, our fear about breaking out

of its zone was because back then it was all Y ratio down to 7050.

Needless to say, the ratios evolve, so

in the two weeks since our last comment you can see how much it has changed by

just comparing the two tables above.

It hasn’t quite got down to 7150, and it

would be nice if it did, but after the SPX got as low as 2825.39, incredibly

close to where we had our R1 and an astonishingly close call considering we

stated that was our level for the bounce when that market was nigh on 2900,

before finishing up 11-points at 2881.40, we suspect London has had its chance.

This week it’s the rollover, so the focus should be on recapturing its zone, so our old friends and acquaintances 7350 and 7450 will, or should be, back in the frame this week.

It has been a very long time since we

last commented on the DJX, but eventually we are seeing those daily 200-point

moves we have been expecting.

Of course, this was back in the last

expiry, but as you can see from the above table the zone is still huge, so naturally

we would be expecting the same in the May expiry.

The interesting part though, has been

how close it has stayed to the centre of its zone, namely 26500, as in two

entire weeks the furthest it has strayed is the measly 200-points.

Worth noting, the last fortnight closes

in chronological order were, 26511, 26656, 26597, 26462, 26543, 26554, 26592,

26430, 26307 and 26504.

And we are already at the mid-point of

this expiry, so the rollover actually starts next week, so we rather doubt

things will remain so unadventurous.

Also, worth noting, is this index is

very similar to the SPX, in that there is an awful lot of Y ratio should it

test and breach its zones lower boundary.

This makes 2895 and 26000 both critical

levels.

So, make sure and watch out for confluence, where they both test their respective levels at the same time.

Range: 26000

to 27000

Activity: Average

Type: Neutral

Nb. Comment on 05/10/19

Wow. In a word.

Never ceases to surprise do the ratios

and when we last looked (6th May) we thought the zone was

ridiculously wide then, so we just don’t have the words to describe what it is

now.

Obviously, since our last comment, here

in the DJX the crucial level was 26000, being the bottom of the zone back then,

so Tue and Wed price action was very important.

The close on the 7th was

25965, so right on the boundary, and, as it turns out, crucial it was those few

points on the wrong side.

Wed saw an intraday high of 26118, so

nice try, but the close at 25967, again shows it on the wrong side, albeit

just.

Of course, now it’s no longer an issue,

and this index has an astonishing 2000-points of zero ratio to play around in

now.

So, basically strap yourself in, as this

combined with the rollover next week, means for us, quiet it won’t be.

Perhaps worth pointing out that activity is high because the benchmark is still exceedingly low, although with such a wide zone that’s pretty obvious.

Well it has certainly been bit of a

quiet start to the May expiry, although things could become far more

interesting now the market is just below a test of R1.

The only change in the ratio above the

zone is Y2 comes in ever so slightly.

Below the zone there are two changes, Y2

comes in to 2815 and R1 to 2775.

However, neither of these are

significant enough to change the overall picture as there is still a sea of

minimal Y ratio below the zone that stretches for 120-points.

Don’t forget, when you add in the zone

itself and the Y ratio above it that is another 60-points.

So, the fact remains, this market

remains very susceptible to any shocks, to the tune of almost 6%.

First things first, and a test of R1 at 2955 would go a long way to establishing what this market really thinks, as bumbling around in the Y ratio like it has been, doesn’t mean anything, well apart from a large degree of apathy.

Range: 2905

to 2955

Activity: Moderate

Type: On balance bearish

Nb. Our comment on 05/09/19

A lot has happened since our last note,

most notably was the test of R1 at 2955, with the intraday high of 2954.13 on

the 1st May, followed swiftly by someone saying “boo”.

For those that had taken a note of our

last ratio table then they would have seen the normal pattern emerge.

Being, down to the middle of the zone,

intraday low 2900.50 before a decent recovery, but knowing where R1 was, not

going there again.

Then, this week it has all been about

the zone, intraday low on Monday of 2898.21 was a test of the lower boundary,

please don’t forget the Vega as the open was nigh on the upper boundary and

that represented a drop of 36.75-points in itself.

2895 and 2905 saw considerable action

the next day, but didn’t provide any highs or lows.

The most significant aspect that day was

the close at 2884.05, just a smidgen shy of their lower boundary, but still a

close in bear territory (i.e. below the zone).

Reinforced by the intraday high on the

following day, Wednesday, being 2897.96, a valiant but ultimately a failed

attempt to recapture the zone.

Which brings us neatly around to today,

and it is really good to see the ratios below the zone improving, and perhaps

no surprise the intraday low yesterday was 2873.28.

This makes Y2 critical today of course, but for us, our eyes are on the corresponding R1 ratio level now at 2815, as that for us will be key.

Nb. Our comment from 04/26/19 (Not

published online)

Despite the fact we last published on

the 15th here in the FTSE it has only been seven trading days, but,

of course, in those seven we have started an entirely new expiry, May.

The fact that this market is inside its

zone is a very good thing we feel, giving it room to breathe and move, without

having to test any ratio levels.

It was interesting to see the intraday

highs on the first two days of this expiry being 7528.93 and 7523.79, which, as

you can see from the table above, is tantalisingly close to a test of R2.

This is made all the more significant as

that is a big jump from the minimal Y ratio straight into the mid R ratio,

which don’t forget are exponential.

The real aspect to watch out for is any

breach of the bottom boundary, at 7350, as that is an awful lot of Y ratio

below there.

All the way down to 7050 in fact, a

rather worrying 300-points.

Also, noteworthy, is the similarity to

the SPX, in that there is a lot of Y ratio below their zone as well.

Activity, especially for May, and it being an intermediary to intermediary expiry, is surprisingly high, but, overall, it is still a very lopsided expiry and one that is still very underdeveloped.

Range:

7350 to

7450

Activity: Very strong

Type: Neutral

Nb. Our comment on 04/30/19

Already it seems the zone here in the

FTSE is having a major impact.

On Friday last week the intraday high

was 7442.39, and we are more than happy to call that strike one of the zones

upper boundary.

And, yesterday, the market basically

camped out on it for the last two and a half hours of the trading day, so

definitely strike two.

For the record the actual intraday high

was 7456.49.

Interestingly, the ratios above and

below the zone have slipped.

Below R2 slides to 6900, whereas above

both R3 and DR move out by 50-points.

Nevertheless, the situation remains the

same, as in we believe the best place for this market is in its zone (7350 to

7450), as above it R2 is still waiting to ambush it at 7550, whereas below we

don’t even see the R ratios start until 7050.

So, all in all, if it can hold within its zone, we think it will be doing well, as if it gets aggressive it could easily get a bloody nose, and if that shakes loose the bears then it is a long way down before it will find any ratio support.

Nb. Our comment from 04/25/19 (Not

published online)

As this is our first coverage of the May

expiry there is no previous comment.

However, in our final comment for April

we stated “Our money is on it shifting to

2895-2905, as back at the start of this expiry this was R2, nudging on R3, so

that is a precipitous fall in the ratio down to Y1”, in respect of the

zone.

So really there should be no surprise

where May’s zone is, or the fact the expiry last Thursday was 2905, right on

the upper boundary.

As we said back then, the SPX does not

seem to have any emotions, bullish or bearish, it seems to be curve-fitting

more than anything else.

However, in doing so it has just made

the situation even worse, as there is now even more minimal ratio below the

zone.

Of course, it needs something to cry

“BOO!” and catch the market by surprise, but if that does happen then it is

worth being aware that R1 below the zone doesn’t even appear until 2770, well

over 100-points away.

It remains to be seen if this index will resume knocking on the door of R2 as it hasn’t even tested R1 at 2955 yet, and we suspect, this will depend on whether either of the other two have an agenda this trip.

Range: 2905

to 2955

Activity: Good

Type: On balance bearish

Nb. Our comment on 04/29/19

Well it has certainly been bit of a

quiet start to the May expiry, although things could become far more

interesting now the market is just below a test of R1.

The only change in the ratio above the

zone is Y2 comes in ever so slightly.

Below the zone there are two changes, Y2

comes in to 2815 and R1 to 2775.

However, neither of these are

significant enough to change the overall picture as there is still a sea of

minimal Y ratio below the zone that stretches for 120-points.

Don’t forget, when you add in the zone

itself and the Y ratio above it that is another 60-points.

So, the fact remains, this market

remains very susceptible to any shocks, to the tune of almost 6%.

First things first, and a test of R1 at 2955 would go a long way to establishing what this market really thinks, as bumbling around in the Y ratio like it has been, doesn’t mean anything, well apart from a large degree of apathy.

Since our last comment on the 4th

it has indeed been all about R2, which back then was at 2885 as you can see in

the left-hand column in the above table.

Furthermore, exactly as we also said

back then (please see above comment), this ratio was slipping, so if you had

taken notice then all the price action in this index over the last week would

have been perfectly understandable.

The top of the DJX’s zone was 26500, and

their intraday high, and so far, expiry high, back on Friday 5th was

26487.

So, taking yesterdays close the DJX has

lost 344-points, whereas, here in the SPX, it is down just 4.92-points.

As we said “it just keeps banging on

that (R2) door” and we even mentioned 2995, so really you just can’t get better

than that.

What we did get wrong however, was that

the rollover and expiry wasn’t “next week” it is now next week.

But worth noting that R2 is now 2925,

but there is what we call a step-up at 2905, which was R2 in-between

publications.

The SPX has laid out its stall, and we

believe it will still be sensitive to a still receding R2, so, for us, it all

now boils down to the DJX, and the top of its zone, and the NDX.

The fact that the rollover and expiry are large on the horizon also means this market is still very susceptible to anyone saying “boo”.

Range: 2805

to 2885 or 2885

to (2905) / 2925

Activity: Poor

Type: On balance bearish

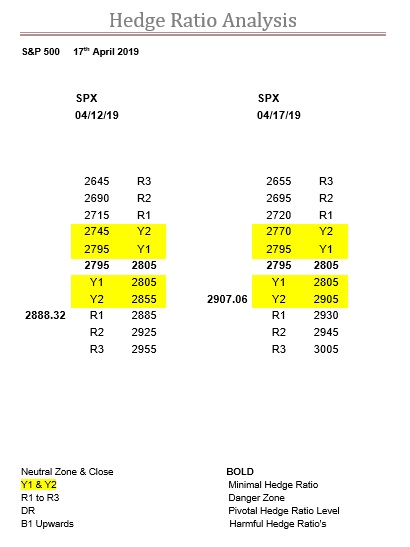

Nb. Our comment on 04/17/19

Well it never really managed to become

as courageous as it was, and therefore never really challenged R2 again.

In our last note R2 was at 2925, and as

you can see today it has barely shifted, now residing at 2945.

Nevertheless, in the intervening period,

the highest this market has got was intraday and 2916.06.

But, although R2 hasn’t moved much, the

really significant move has been the huge expansion of the Y ratio bandwidth,

which now stretches all the way up to 2930.

The fact the ratios have hardly filled

in underneath, means this is more by default, or by a distinct lack of interest

either way really.

The end result, is that the zone could

easily flip to anywhere in the Y1 ratio bandwidth, and probably even Y2, the

ratios are receding so fast.

Our money is on it shifting to

2895-2905, as back at the start of this expiry this was R2, nudging on R3, so

that is a precipitous fall in the ratio down to Y1.

Admittedly, this index has been knocking

on the R2 door, each time forcing it higher, but it hasn’t really filled in

underneath, and leaving the zone to move right at the end is more about

curve-fitting than rampant bullishness.

So, this index is still very scarily susceptible to anything going “boo”, but in the absence of such it is in default mode, trudging higher without any conviction that we can discern. In fact, quite the opposite.

And we were not wrong as 7250 dominated

this index for that week, until Friday 29th when it managed to hold

on for that all important close above it, at 7279.17.

The trouble is that when we last

commented on the FTSE, an entire 10 trading days ago, the ratio landscape has

transformed.

There is absolutely no point in guessing

when, so we are just going to fast-forward to the end of the next week, Friday

the 5th April, when the close was 7446.87.

More importantly, the intraday high was

7461.39, so we strongly suspect that was this index’s first pop at R3.

However, we would be remiss not to point

out how huge the changes have been, and in fact, so much so, they have

virtually flipped 180 degrees from the 25th March.

Although there is now Y2 above the zone,

what was there back on the 25th is now below the zone, which itself

has leapt 200-points to 7150-7250.

But, the real clincher, is B1 has gone

from above the old zone to now being below it, which signifies that the entire

ratio alignment has totally adjusted.

No wonder it has managed to eventually

achieve what it was threatening to in that very first week.

We would fully anticipate 7450 to slip

to R2, leaving 7500 as the next resistance level.

If this is the case then the trading

range should be 7400 to 7500.

Then, it will be all down to the rate of change in the ratios, especially as the clock is ticking and the expiry is now fast appearing on the horizon.

Range:

7400 to

7450 or 7450

to 7600

Activity: Average

Type: Bearish

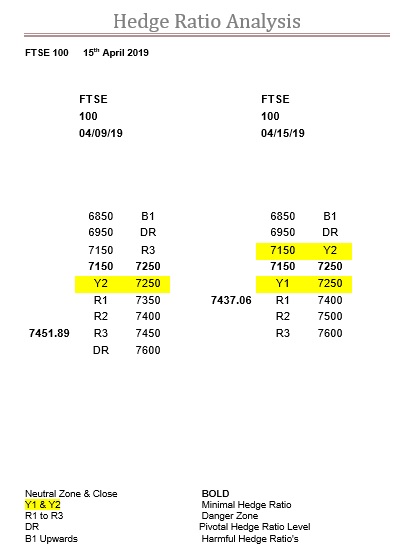

Nb. Our comment on 04/15/19

Well when we made our trading range just

7400 to 7450, we thought the ratios would change sooner rather than later but

it held out all week.

This made last week one of the quietest

this year, with the net move on the week of just minus 14-points.

Despite 7450 getting battered all week

it held, but as you can see R3 has now slipped to 7600, and our trading range

is indeed now 7400 to 7500 just as anticipated.

However, the market is now out of time

as we enter the rollover and expiry, which this week is on the very unusual

Thursday.

This means 7400 is the really critical

level, as below it is now all just Y1.

The good news is, as the ratios have

fallen so far, that the zone is very likely to move up again.

But, even so, the market is still way ahead of where the zone may end up, so it’s going to be an interesting week for sure.