We just hope

you were listening, as way back on 21st January, at the very start

of this expiry, in the FTSE we said; “So, that means, at the moment, there is

precious little ratio from 6750 all the way up to 7050”.

6750 was

also R1, and the intraday low on 28th Jan was 6734.00.

Today, the

corresponding R1 is lurking at 7050, just waiting to ambush this index.

Worth noting

is that this is backed up with R2 at 7100.

The even

better news is that we are only just at the half way point in this expiry.

Apart from just being aware of the ratios in the FTSE it is also worth taking note of where the DAX and the US indices are in relation to their ratios.

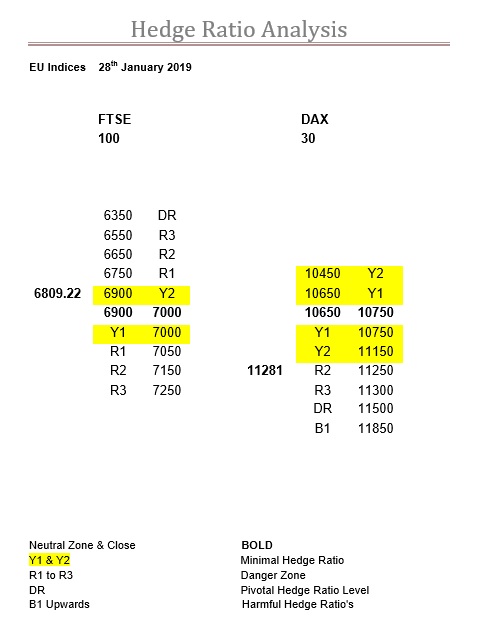

Range: 6750

to 7050

Activity: Average

Type: On balance bullish

For the DAX

we couldn’t have been more explicit, and again from the very start of this

expiry, back on the 21st Jan, when we pointed out the zone could be

anywhere in the Y1 ratio bandwidth, and the presence of R2 and R3 at 11250 and

11300 respectively.

So, no

surprise the zone has moved to where it is.

Also, no

surprise the intraday high and, so far at least, the expiry high, back on the

25th Jan, was 11321.

In fact,

since that high the DAX has fallen 141-points.

To put this

in perspective the FTSE since the 25th has risen 211-points, a very impressive

350-point divergence.

Two main

points to be aware of here, the first is that R3 has slipped to 11450, while

the second is that there is still a huge amount of Y ratio still present.

The activity has also diluted somewhat the “every man and his dog” bullishness, and if this does crack, then this index is still on the edge of a Y ratio precipice.

Just to

remind everyone what we said last week about the FTSE; “firstly, the zone, and although it has dropped to 6750-6850 it could in

fact be anywhere between where it is now and where it was last week…. So, that means, at the moment, there is

precious little ratio from 6750 all the way up to 7050”.

Therefore,

the fact the zone today has moved to 6900-7000 should not come as too much of a

surprise.

Nevertheless,

it is worth remembering that it was 6750-6850, as the close last Wednesday was

6842.88, and the last two intraday highs have been 6854.59 and 6858.19 on

Thursday and Friday respectively.

Obviously,

the zone will have an impact, so it should definitely be taken note of, but the

situation remains much as it was, with little or no ratio from 6750 up to 7050.

The fact that the zone kept the FTSE in check last week runs slightly contrary to the high level of activity, so we can only see things getting more and more animated as this expiry progresses, and especially so now the zone has moved.

Range: 6750

to 6900

Activity: Very good

Type: Neutral

Carrying on

with the “what we said last time” theme, here is it for the DAX; “today, will be the decider we feel, as the

proof will be how this market reacts to the R ratios at 11250, and especially

at 11300, so, best also pay close attention to any opening gaps”.

When we

wrote this the DAX had just jumped 286.92-points to finish at 11205.

The market

actually gapped down at the open on the Monday and it wasn’t until Friday that

it managed to get back to where it was.

In the

meantime, neither R2 or R3 haven’t moved, so it is going to be a definitive

Monday with this index camped on the R3 doorway.

Actually, it

was very interesting to see how it coped with R2 at 11250, as after all that Y

ratio it must have been bit of a surprise to walk into that futures selling

generated by the dynamic delta.

It is very

aggressive, and, again, as we said, “every man and his dog” here are bullish,

but make no mistake, they will now have to seriously work hard to achieve their

ambitions.

And, please bear in mind, if it does go sour, there is nothing but minimal Y ratio below, so it could be “calamitous” with virtually no ratio support at all underneath.

Even though

the US markets were closed on Monday we still expected a bit more zip out of

them during the rest of this week.

Especially

considering what we said about the SPX in our last comment; “although, the Y ratio bandwidth is

considerably thinner, it is still absolutely massive”.

However, the

ratios have been evolving, and we are seeing some good strengthening below the

zone and some weakness above it, which is bullish.

To highlight

this, we have lost Y1 below the zone altogether, whereas above it Y2 now starts

at 2655, and more importantly R1 slips from 2670 to 2680.

This is

significant, as on last Friday the intraday high was 2675.47, and it has

noticeably not gone near there since.

The way it

is going also means we may well see a move up in the zone to 2645-2655,

competing the bullish triumvirate.

At the end of the day, we think it is the DJX that is going to be the deciding factor, so read what we say below first, then apply it to what may happen here in the SPX.

Range: 2605

to 2680

Activity Moderate

Type: On balance bearish

As we said in the NDX; “so,

don’t take those ice-skates off any time soon”.

Activity remains low, but basically the benchmark is so small,

by just achieving what they have done, it is actually rather pathetic.

Nevertheless, it hasn’t stopped them adding about 50 new

strikes.

No problem if it stimulates interest, but it plainly doesn’t, so

why bother?

Y2 below the zone has come in a fair way, but at the end of the day it is still all Y ratio, so enjoy the skating.

Range: 6425

to 6825

Activity: Average

Type: On balance only just fractionally bearish

We certainly

“bigged up” the DJX in our SPX comment above, and for very good reason.

In our last

comment about the DJX we mentioned; “therefore,

for this expiry, 24600 is a really key level”.

And the

market must have been listening, as that very day, Tuesday 22nd, the

DJX opened at 24607, which also became the intraday high.

The next day

it had a very aggressive test of its zone, peaking at 24700 and falling as low

as 24307, both rather coincidentally being 100-points either side of their

zones upper and lower boundaries.

However,

yesterday was a bit more precise, with the intraday high of 24626, and intraday

low of 24422, making this a near perfect zone bandwidth test.

To be fair,

we would count both as zone bandwidth tests, so today fully expect a breakout.

The bandwidth

test alone suggests it, two in a row, double hint, and on top of all this,

another test would be strike 3 anyway.

The SPX

certainly paints a better picture than when we looked at it back on the 15th

Jan for the rollover.

Although,

the Y ratio bandwidth is considerably thinner, it is still absolutely massive.

Currently,

it stretches from 2495 all the way up to 2670, which is, naturally, where this

index came to rest last Friday, being closed Monday.

So, it is

still 175-points (6.6%), and this seems to be the way of it these days, as just

having a 1% to 2% Y ratio bandwidth is but a distant memory.

Therefore,

it will be a real test of this index today, whether it wants to take on the R

ratios from the off, or take advantage of this huge bandwidth.

Nice to see a start to a new expiry begin with it all to play for, and worth noting is the very decent level of activity, which means a respectable degree of engagement.

Range: 2605

to 2670 or 2670

to 2715

Activity Strong

Type: On balance bearish

Sadly, we never did the rollover for the NDX.

This means our last coverage was way back on the 8th

Jan and considering Y2 then didn’t kick in until 7125 we are not really

surprised by what happened.

Although we have no idea how the tail end of the last expiry

developed, if indeed it did at all, but we do recognise that what we are seeing

here is exactly the same as what we saw this time last expiry.

So, don’t take those ice-skates off any time soon.

Perhaps worth noting that the intraday high on Friday was 6816.23, so they may well already have an inkling of where Y2 in Feb is.

Range: 6425

to 6825

Activity: Average

Type: Neutral

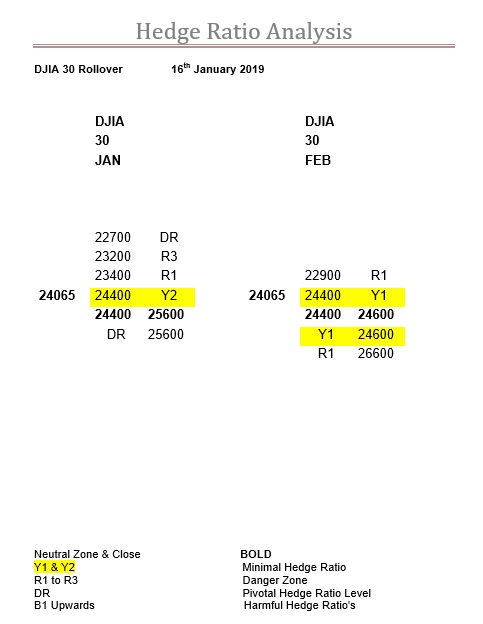

In the Jan

expiry just gone the SPX got its way on the rollover Wednesday, which left the

DJX here, free rein for the actual expiry.

Suffice it

to say the zone in both Jan and Feb have not changed, and the settlement price

on Friday was 24574, so we would say spot on really.

Who would

have thought, that after all that trouble getting over 24100 and back into

their Y ratios, that they would eventually succeed come the expiry, so bravo

the DJX.

Despite the

level of activity, sadly here the benchmark is so low anything looks good,

there has been little change in the ratios since we last looked.

In fact, the

ratios are so thin, the zone could actually stretch from 23900 all the way up

to 24600.

Therefore,

for this expiry, 24600 is a really key level.

Unless the ratios start getting populated this is going to be a real rollercoaster ride this expiry, so either hang on tight or sit back, enjoy, and wave those hands in the air.

When we last

looked at the FTSE the zone in January was 6800-6900 and in Feb it was

6950-7050.

On rollover

Wednesday, the FTSE closed at 6862.68, close enough to the middle of the zone,

and the close of Friday, as one can see, would have been where the zone was, so

job done really.

Now, we come

to where the ratios and the zone are now.

Firstly, the

zone, and although it has dropped to 6750-6850 it could in fact be anywhere

between where it is now and where it was last week.

So, that

means, at the moment, there is precious little ratio from 6750 all the way up

to 7050.

When you add

the Y ratio at either end then we have the potential to have a great expiry

with trading range of 350-points, or just over 5%.

Enjoy.

Range: 6850

to 7050

Activity: Outstanding

Type: On balance only just bearish

Boy, do we

now regret not doing the rollover for the DAX.

Our last

comment on this index was back on the 7th Jan, when the market had

just closed at 10767.

This is

worth recalling as the zone then, for the Jan expiry, was still at 10950-11050,

so last Wednesday, the rollover, when the market closed at 10931, we thought

job done.

However, and

here’s the regret, we had no idea how bizarre Feb was shaping up to be.

As one can

see from the table above, the ratios are seriously lopsided, and more

interestingly the zone is down at 10650-10750.

However,

where the zone is concerned, it could very easily flip to anywhere in the Y1

ratio bandwidth.

And that’s

the issue here, as Y ratio is all there is under the zone.

It may not

go sour, and the delta ratio of 500% suggests every man and his dog thinks it

won’t, but if it does, it could be calamitous. Unless you’re a bear of course.

Today, will be the decider we feel, as the proof will be how this market reacts to the R ratios at 11250, and especially at 11300, so, best also pay close attention to any opening gaps.

DJX Jan to Feb Ratio Rollover Table 16th January 2019

For the DJX this expiry it was all about

23400, which we have covered at great length in previous articles, but once

over that hurdle and into its Y ratio bandwidth we mentioned two other hurdles

in its way.

“We call them “step-ups” and here there are two in this mammoth

Y ratio bandwidth, at 23800 and 24100”.

As yesterday’s intraday high was 24099

it is this second one that has caught our attention.

Today is the day of course, and the SPX

being anywhere in the vicinity of 2600 is job done to us, which leaves the DJX

quite a bit shy of theirs.

Now, the problem with getting over 23400

certainly held this index back, thereby increasing the disparity.

Furthermore, it is in Y ratio, so not

that painful, but 24100 is quite a hurdle, and once the SPX has had its way our

fear is that this index may look towards somewhere circa 23600 as the next

cheapest alternative to expire around come Friday.

As we have all expiry, we still feel the DJX is the kingmaker, so it will be the one to watch right to the end for sure.

Range: 23400

to (24100) / 24400

Activity: Moderate

Type: Bearish

To be fair this is now becoming bit of a

theme, the Feb DJX being like the FTSE and SPX with little or no ratio in situ

at this moment in time.

Intermediary to intermediary or not this

is unusual.

Pointless to speculate why, it may be

for different reasons in each market, or everyone could simply be heading for

the hills, and we don’t mean to go skiing, we just see the end result.

The fact that the Y1 ratio bandwidth

here stretches for 3700-points is bad enough, but this is not the entire story.

Basically, the zone (zero ratio) could

be from 23400 all the way up to 24600.

So huge potential for extreme volatility

and whipsaw.

This, for you, may be a good thing of

course.

If the market blasts north no doubt the

politicians will take full advantage, but make no mistake, this index is very

vulnerable with no ratio to support it.

If it skids down to 23400, we rather doubt

the seriously minimal Y1 will have much, if any, impact, and if it then carries

on to 22900, will R1 be enough?

It was a truly awful end to 2018 and at

this very point in the Dec expiry we were using the analogy of it escaping from

under the pile-driver it was trapped beneath.

The net result was the Jan expiry opened

with an unprecedented bandwidth of Y ratio, a truly astonishing 350-points

wide.

It still didn’t stop the SPX from

testing R3 at 2345 with the intraday low of 2346.58, which, so far, is the

expiry low as well.

The fact the market responded, and quite

emphatically, finishing up 117-points that day at 2467.70, revealed it had

broken free from the pile-driver, courtesy of the new expiry no doubt.

Rather intriguingly the Y ratio

bandwidth has stayed incredibly broad, so it has the opportunity to cut loose,

but the DJX was quite a limiting factor.

The fact that their zone is hovering

near the market, or vice versa, we suspect means they want a quiet expiry.

Good luck, is all we can say, as the Y ratio bandwidth still stretches from 2470 all the way up to 2685, so from our perspective anything can happen under these circumstances.

Range: 2570

to 2580 or 2580

to 2605

Activity: Poor

Type: On balance only just bullish

Don’t forget we do not make the rules,

just report the numbers.

This is, in fact, the essence of the

problem, as there are no numbers.

It may well be that one of the other two

step up and take charge, but as things stand here in the SPX it certainly won’t

be this index doing that.

Intermediary expiries to intermediary,

apart from being the least common, tend to be noticeably underrepresented, but

this is going way past that.

The fact is that the zone is a little

bit higher, but the minimal Y1 ratio is so minimal that it could be the zone in

its entirety.

The Y ratio bandwidth “is only”

290-points wide, so less than Jan at this stage, but this is still ridiculously

wide, and, more to the point, there is no depth.

On both sides the ratio only goes as

high as R2, at least last expiry we saw some DR.

Still a few days to go, but skittish doesn’t go anywhere near enough to describing how this index may be in the Feb expiry, and that’s in either direction.

Well it certainly has been a nomadic

zone for the Jan expiry in the FTSE.

In fact, it has changed every time we

have commented, which is actually a reflection on how very low the already minimal

Y level of ratio really is.

This then has led to the fact the zone

could be anywhere from 6650 to 6900.

Of course, this expiry we have already

plumbed the depths of 6536.53 where it took a colossal effort by R3, then at

6550, to turn the tide.

We did mention, that on the flip side,

resistance may be more sensitive, and we have already seen this market test R1

at 6950.

Now, this index is tantalisingly close to its zone, and with just two days to go to the rollover it will be a very nervy time.

Range: 6900

to 6950

Activity: Poor

Type: Neutral

We look at the calendar every day but

still the fact it’s the rollover already comes as a surprise.

Doubly so as it has been a very hectic

start to the year already.

Therefore, we suspect, a bit like us,

many participants have been blindsided as this must be the poorest

representation of ratio we have ever seen in the FTSE.

Of course, with March just around the

corner, then it will not be helped with many sitting on their hands as well.

When you couple this with the fact this

is the first, of only four, intermediary to intermediary expiries, then this

just compounds the lack of ratio.

So, what we say above, about a nomadic

zone, then this expiry is not going to be any different.

In fact, if, and that is a very big if,

this index suddenly develops a degree of sensitivity, then it might just trade

within the Y ratio bandwidth.

However, when one realises that this

bandwidth is 650-points wide then one will also realise that R1 will be very

hard pushed to reverse a market that has that much momentum behind it.

And so far, that is pretty much as high

as it goes, scarily.

Seems like the Jan expiry was just the warm-up act for this the Feb expiry.

It’s not a

big change in the SPX, more of interest than significant as well.

The zone has

moved up to 2545-2555, and normally we would comment on this being like taking

a super tanker through a three-point turn in a country lane, but the phenomenon

of 290-points of minimal Y ratio makes this not the case, and in fact rather

mundane.

It is

perhaps worth noting, that this move up does put the market inside its zone, so

in neutral, rather than above it, and therefore in bullish territory.

However,

with so little ratio about you can pretty much guarantee two things; firstly,

volatility, and secondly, a nomadic zone.

Please don’t forget this index has already tested R3 at 2345 this expiry, so is 8% up from its low, and with virtually two weeks to go, so the bears may not be squealing yet, but time is now not on their side, and the R ratios above the zone still don’t even appear until 2725, so the final battle for this expiry is still to come we suspect.

Range: 2545

to 2555

Activity Very poor

Type: On balance just bearish

For the NDX no change in its zone, but rather intriguingly no

further additions of any strikes.

Although activity has improved, it really isn’t worth writing

home about.

Especially, when one considers that it is very stunted overall,

so a little goes a very long way and yet this was the best it could do.

It did have fun around its zone, closing in it and bouncing off it, but at the end of the day the minimal Y ratio is actually very minimal, and what’s more, there are no step-ups, so it really is just one exceedingly vast ice-rink.

Range: 6275

to 7125

Activity: Moderate

Type: On balance only just bearish

It is difficult

to emphasise strongly enough how significant a level 23400 is, and has been,

and not just for the DJX, but also for the other two US indices, and by default

the European exchanges as well.

The first

encounter was on the 28th Dec with the intraday high of 23381, and

when it was R2, which turned a 250-point gain into a 76-point loss.

It shied

away from it on New Year’s Eve.

But attacked

again on 2nd Jan with the intraday high of 23413.

The next day

saw that 660-point fall.

By the 4th

it was now R1 and the bulls were emboldened again, courtesy of the SPX and NDX,

and it made a good intrusion but finished right on it, despite this being

strike 3 and a lot weaker.

And,

yesterday, it didn’t have it all its own way, but finished on the right side,

if you are a bull, so hopefully job done, but the heavy weather it made of it

does not inspire confidence for sure.

As we say

above in the SPX, we suspect there the deciding battle is still to come, so we

are certain that here there will be one here as well.

We call them “step-ups” and here there are two in this mammoth Y ratio bandwidth, at 23800 and 24100.

Hope you

were listening in the FTSE as “obviously,

there is still considerable risk, but now we are into a new expiry, and if it

can get back above 6750, then it could become a very rapid ascent up through the

zero-ratio zone to 6900”.

The intraday

high on the Wednesday and Thursday was 6753.29 and 6753.14 respectively, so

Friday would have been strike 3.

However, the

fact that the zone has changed, and the intraday high and low on Friday was

6850.37 and 6692.50, we suspect that this change happened on Friday.

Again, these

ratios should be calculated daily, as that is almost the perfect zone bandwidth

test, 6700 to 6850.

We say,

almost, but really seven and a half points on a six-thousand-point index, that

traded 150-points in one day, is probably the closest you will get to perfect.

Basically, a

drawdown of 0.11%.

This should

result in a breakout today, the only caveat is the DJX, which if you read our

note on Friday you will appreciate how significant 23400 really is, and the

close was above it, but only just, and that is a very large index, so 33-points

is only 0.14%, which is rather ironic considering the above.

For the

FTSE, obviously 6850 is a poignant level, but if it gets above that then there

is still plenty of Y ratio above for it to play around in.

Although, due to the nervousness still embedded in this market, we rather doubt it will be the corresponding R3 ratio (intraday expiry low 6536.53 with R3 at 6550) so be rather wary circa 6950.

Range: 6700

to 6850

Activity: Poor

Type: Bullish

There were

two things we said in our last comment on the DAX that are worth repeating, “this makes 10600 very significant” and “it was the level of activity that caught our

eye”.

The very next

trading day the intraday high was 10612.

Also, as you

can see below, that despite all the closures here over the festive period they

have still maintained a very impressive level of activity.

Of course,

not calculating the ratios daily coupled with a lot of closures makes any form

of continuity here rather difficult, but despite this it has been fascinating

to see their zone hold fast.

When this

index was heading towards 10000 this looked misplaced, but after yesterday it

doesn’t look so awkward anymore.

Using a

broad brushstroke, the two pertinent levels over the last two weeks have been

10450 and 10250, and although the ratios may have fluctuated a little bit they

have stood out, and actually over the last two weeks been counted as well.

The Y ratio bandwidth may have shrunk a bit, but it is still a very impressive 650-points, so don’t expect any quiet days anytime soon.